TankerLandia — December 2022

A round-up of crucial news, with a focus on Russian oil trade dynamics

December 2022 has been an unusually eventful month for oil tanker-related news. I document what’s happens via Twitter, day by day. I thought it would be helpful to “zoom out” now.

On 1 December, BRS calculated that Russia and its allies would have enough tankers to ship its oil close to pre-cap levels. This turned out to be incorrect, as admitted by Russian government officials a few weeks later. (more on that below).

Another important dynamic was the anxiety of traders vis à vis Russian oil, leading into the price cap deadline of 5 December 2022. The uncertainty led to an even greater discount for Russian crude, as the small pool of buyers temporarily became even smaller. On 1 December, Argus estimated at 35% discount for Urals:

A day later, I stumbled on the news, cited in Russian media Kommersant by a government official, that China was refusing to recognize Russian insurance:

These was a panic until the Central Bank of Russia (CBR) decided to recapitalize the Russian National Reinsurance Company (RNRC)… i.e. the Russian Central Bank became the guarantor for the RNRC, making its authorized capital “almost unlimited” according to Deputy Minister of Transport Alexander Poshivay (h/t Ben Aris of BNE Intellinews).

Soon afterwards, Bloomberg said freight costs could reach as much as $20/barrel for loadings after 5 December, well over double the norm. $29.50/barrel discount for Urals (see above), freight costs of ~ $20/barrel… at this point it’s becoming clear that the discount is being eaten up by higher shipping costs.

Increasingly it became clear that the bigger Chinese state refineries wouldn’t touch Russian oil, but that smaller independent “teapot” refineries were tacitly being allowed to import Russian crude via oil traders, who insisted on “delivered” contracts, i.e. delegating the responsibility of shipping with the seller. Always pragmatic, those Chinese…

On the same day, the Indian Minister of Petroleum made an open, sweeping commitment to continue to buy Russian crude, including after the introduction of the price cap, which must have been a relief to Russia, as most countries adopted a “wait and see” approach (I’m looking at you, Turkey).

From interviews U.S. Treasury Secretary Janet Yellen gave leading up to the price cap deadline, it became clear that the U.S. government not only was aware of India’s intention, but wholeheartedly encouraged it, as it allowed Russian oil to flow, which helped avert a spike in oil prices, all the while implicitly decreasing Russia’s revenues because a discount was necessary to make up for the higher freight costs (India is farther away from Russia’s Baltic ports than Rotterdam…)

This is superbly illustrated in a slide from an Argus presentation:

The New York Times, which frankly has lagged in its coverage of this story, versus the Financial Times, Wall Street Journal, and domestic Russian media, nonetheless highlighted an important mechanism which might allow Russia to bypass the price cap: (can you say “barter”?)

China’s bilateral trade with Russia has increased greatly in 2022, but it is clear who has the leverage in the relationship:

Based on statistics from November imports, it started to become evident that Russia needed to find new customers, or about 1m barrels per day would not find buyers. This is something which has still not been resolved, over three weeks later, although presumably the Russian government is working behind the scenes to find new trade partners in Asia, Latin America, and Africa. Expensive shipping costs would certainly affect trade with the latter two.

At this point (4 December) we started seeing the first signs that the price cap on Russian petroleum products is going to be MUCH messier than the one on crude, simply because there is such a diversity of products and prices, which vary daily:

An earlier rumor, which never materialized, was that Indonesia might be a buyer of Russian crude oil, if the price was right. But I never saw any follow-through:

While ~27% of the world tanker fleet could be available to transport Russian crude, in theory, in practice it seems like there are not enough vessels willing to participate and run afoul of Western insurance companies (more on that below):

We are now seeing Orrin’s prediction come true: Chinese owned VLCC’s are being loaded with Russian crude via STS (ship to ship transfers) in various locations, including off the West coast of Africa. Which means that the VLCC’s (which carry 2 million barrels of crude each) sail all the way around South Africa, as they are too large for the Suez Canal. A much longer voyage, therefore more expensive, tying up fleet capacity for longer.

On 5 December, we saw the first signs of what became China’s epic Covid pivot:

Sales of older tankers continued to make new highs throughout this period, and everyone knows where those tankers are going… Documented by Cleaves Securities:

As the 5 December deadline approached, OPEC became more openly concerned about major buyers (the US + EU + other allies like Australia, Japan) inflicting pain on producers. The price cap is being perceived as the expression of leverage:

Tankers with the capacity to carry (Russian) petroleum products through icy waters started seeing truly eye-popping bids:

On December 6th Reuters published what has been one of the most thorough investigative accounts of tanker trade mechanics, as opportunistic players looked to capitalize on the extraordinary rates premium for shipping Russian crude. A juicy excerpt is below:

Chinese President Xi Jinping shrewdly scheduled a trip to Riyadh at precisely the time when Russia was most nervous about finding customers for its oil. This allowed Xi to ensure diversity of oil supply (an important point for such a rapacious consumer of oil) while at the same time remind Putin that Russia needs China more than China needs Russia.

During the period, much ink was spilled about the delays in the Turkish Straits, and I predicted that it would not be a big deal:

A short quote from a shipping insider in The Times (UK) summed up what everyone in shipping knew by now: Russian crude would find “creative” ways of getting to market:

There have been conflicting reports in Pakistani media about whether Russia would agree to sell them crude at a discount. Sometimes Pakistani government officials made contradictory statements in the same day.

Meanwhile, the Indian and Chinese market share of Russian crude oil exports became more and more extreme, according to Refinitiv:

Obscuring the origin of Venezuelan and Iranian crude has become big business, and Oil Price documented some of the tricks:

One of the hottest topics is whether or not Russian crude oil production will suffer next year, and by how much. One of the few analysts who thinks that the pressure is overstated is Arkady Gevorkyan, a commodity strategist at Citi Research:

More and more oil tankers loaded in Russian ports are not even bothering to disclose their final destinations:

A useful slide by Vortexa documents the mechanics of the STS transfers:

More evidence that Urals can’t find buyers, and that freight costs have skyrocketed:

Russia started acknowledging reality by setting up sites to transfer oil from smaller shuttle tankers to larger vessels, better-suited to long voyages to East Asia.

Oil traders start to talk more openly about how Russian oil will be blended: one tanker, half full of Russian crude, will be loaded with additional barrels of crude from another origin, before being sent to its final destination. Talk about inefficient trade!

In the meanwhile, Europe has pivoted to other producers of crude oil, all farther away than Russia:

I made this map to help visualize the distances involved:

10 days after the introduction of the price cap, it became evident that Russia was, in fact, tacitly allowing Western insured vessels to transport its oil, in contradiction to defiant public statements by Russian government officials. Great investigative reporting by the Financial Times:

About a month before, I was increasingly berated by experts telling me that European diesel shortages would soon turn into gluts and full inventories. Reality:

After Urals suffering from a lack of buyers, it became the turn of ESPO crude (which is sent to East via pipeline):

India became the biggest buyer of Russian crude, a sea change from pre-war levels:

Despite a huge increase in bilateral trade between Russia and China, China needs to tread carefully to not upset its two much bigger trade partners: the US and the EU (via the Centre for European Reform)

Chinese traders enjoy their leverage when bidding on ESPO crude:

Although I didn’t take the headline of oil majors avoiding tankers which ship Russian oil too seriously (below), as it was stated as a “preference”, this does raise the possibility of self-sanctioning, which has become such a surprisingly potent factor since the Russian invasion of Ukraine.

Russian media Kommersant divulged that Russian refinery utilization is increasing to compensate for the lack of demand for Russian crude (there is no such lack of demand for Russian diesel, Russian jet fuel, etc.)

Owners, many of them Greek, capitalize on the red-hot demand for older oil tankers which, under normal market conditions, would be on their way to the demolition beaches of Bangladesh. In this instance, Delta Tankers (which has been particularly active in Russian ports, pre price cap) sold on four of its oldest vessels at a huge premium, presumably to buyers who will continue using them to trade Russian oil.

The number of countries buying Urals crude dwindles to four:

Oil traders become more chatty about the difficulty of moving Urals:

The bombshell, not entirely unexpected, that the U.S. is allowing for an extra buffer period to unload Russian oil products post 5 February up until… 1 April 2023:

We no longer have to wonder whether Russia has enough oil tankers to ship its oil, because… Putin’s favorite banker tells us they don’t. This also indicates that the demand for older tankers is far from exhausted:

Despite Putin mentioning these territories in recent speeches as possible customers for Russian hydrocarbons, Russia has struggled to find new customers in Latin America and Africa:

My friend Oil Bandit offers a plausible explanation:

I offered a reminder that with a 35% discount, Russian profitability is being compromised:

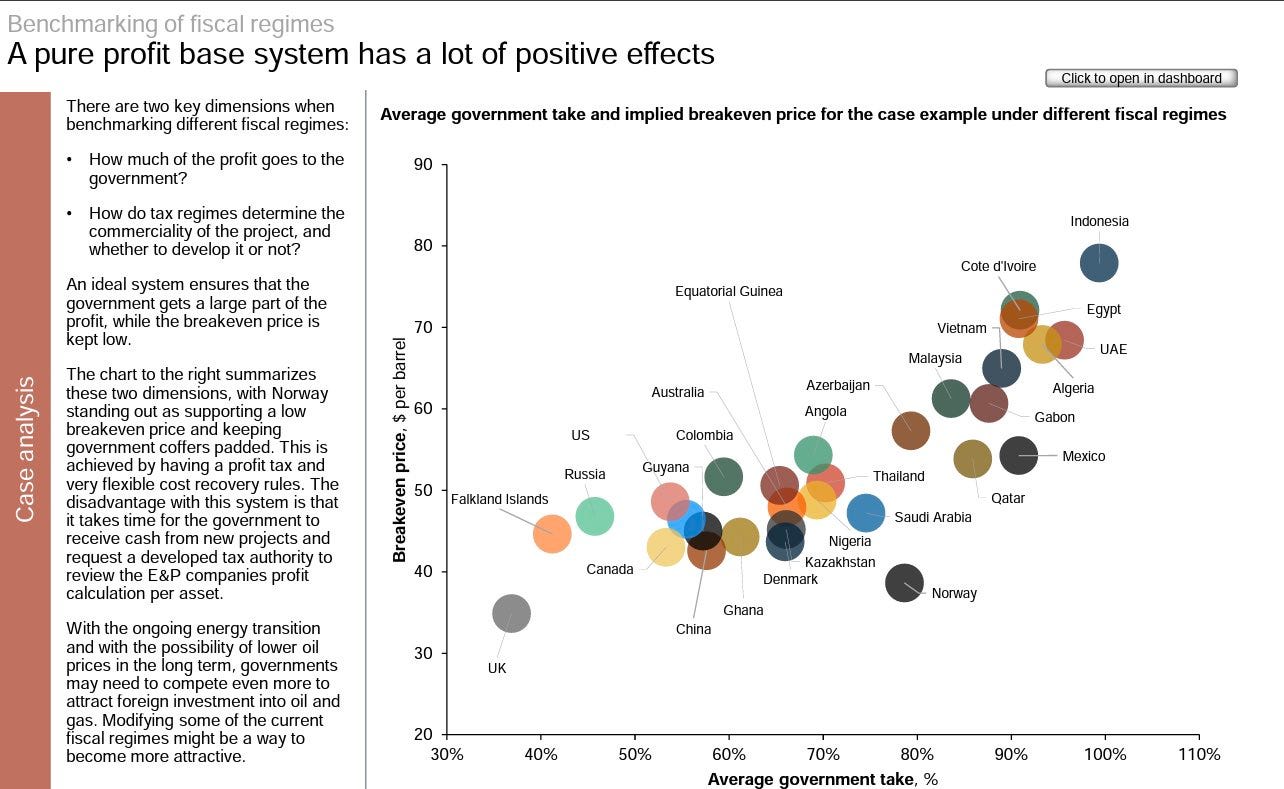

An alternative source (Rystad) shows breakeven prices per oil producer:

And Russian government officials start becoming more forthright about their desperation to find new customers:

Another admission of the mechanics leading to the heavy discount on Russian crude:

As the Russian government had calculated its 2023 budget based on a higher oil price, they admit that they are feeling increased pressure:

One of my favorite little tidbits from recent news, when Sasha Novak complains about a possible buyers monopoly (oligopsony):

After weeks of warning that the Russian government “is planning a response” to the price cap, Putin comes up empty, simply saying they will ban sales to countries which observe the price cap (something he had already been saying for weeks). My interpretation is that Russia did the math, and realized they can’t afford to pull oil from the market while pursuing an expensive war, so they are stuck accepting it, while pretending not to:

There are now rumors that Turkey might be getting skittish about importing Russian oil, but the source is the pro-Western Moscow Times, so I am cautious about excessive editorialization.

Turkish import volumes have not been spectacular anyway. They have greatly risen year-over-over in percentage terms, but in absolute terms Turkey won’t make much of a difference.

What happens next?

Follow me on Twitter to find out! www.twitter.com/ed_fin

Fantastic summary. Thank you for this. I really appreciated it. Cheers John.